The 10-Minute ‘Paycheck Split’ Habit: Turn Every Direct Deposit Into Automatic High-Yield Savings

You know the pattern. Payday hits, you feel a little relief, and then the money starts getting assigned jobs fast. Groceries. Rent. Gas. A streaming charge you forgot about. Dinner out because it has been a long week. Then you promise yourself you will save whatever is left. And somehow, there is never much left. That is not a character flaw. It is just how money behaves when it sits in checking and waits to be spent. The fix is surprisingly simple. Split your paycheck before you can second-guess it. Send a fixed amount or percentage straight into a high-yield savings account the same day your direct deposit lands. Ten minutes of setup can turn your next paycheck into a saving system that runs quietly in the background, without a spreadsheet, guilt trip, or total lifestyle overhaul.

⚡ In a Hurry? Key Takeaways

- The paycheck split high yield savings habit works by moving part of every direct deposit into savings before you have a chance to spend it.

- Start small with 5 percent, 10 percent, or a flat dollar amount, test it for one or two pay cycles, then raise it slowly if your checking account still feels comfortable.

- Keep enough in checking for bills and daily life, and use an FDIC- or NCUA-insured high-yield savings account so your money stays accessible and earns more.

Why saving “what’s left” usually fails

The old plan sounds reasonable. Pay your bills, live your life, then save the leftovers.

The problem is that leftovers are unpredictable. Life does not care that you meant well. A tire needs air. School fees pop up. The dog needs medicine. Your friend wants to meet for lunch. None of these things are huge on their own, but they eat the “extra” money before you ever move it.

That is why automation matters more than motivation. If savings happens first, spending adjusts around it. If savings happens last, spending usually wins.

What the paycheck split habit actually is

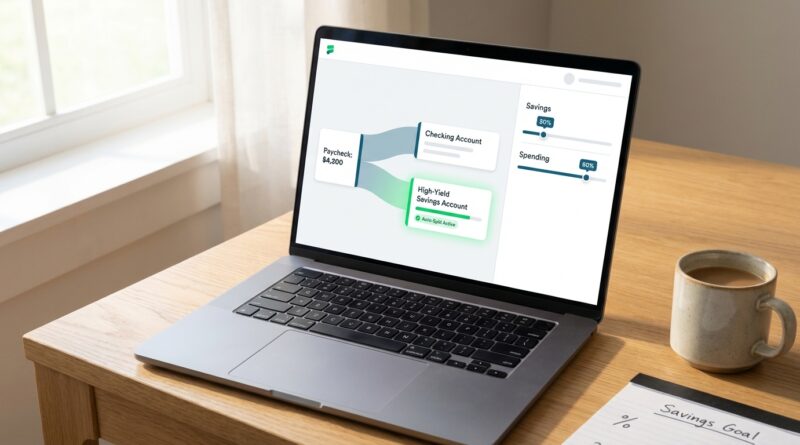

The paycheck split high yield savings habit is exactly what it sounds like. Every time you get paid, a set piece of that deposit goes straight into a separate high-yield savings account.

You can do this in two common ways:

Option 1: Split direct deposit through payroll

Many employers let you divide your paycheck between two accounts. For example, 90 percent to checking and 10 percent to savings, or $150 to savings and the rest to checking.

Option 2: Auto-transfer on payday

If your payroll system does not support split deposits, set an automatic transfer from checking to your high-yield savings account on payday or the day after.

If you like the idea of a tiny delay so the transfer feels less tight, you might also like The 48-Hour ‘Quiet Auto‑Transfer’: One Tiny Rule That Lets Your High‑Yield Savings Grow Before You Even Notice. It is a nice backup plan for people who want a little more breathing room.

Why a high-yield savings account makes this habit better

A regular savings account often pays so little interest that it barely feels worth the effort. A high-yield savings account changes that. Your money stays liquid, meaning you can still get to it if needed, but it earns more while it sits there.

That matters because this habit is not just about hiding money from yourself. It is about making every saved dollar work a bit harder over the next 6 to 12 months.

Rates move over time, of course. Still, when rates are attractive, this is one of the easiest wins available. You are not chasing a risky investment. You are building a cash cushion that earns something real.

How to set up your split in 10 minutes

Step 1: Pick your starter amount

Do not start with the biggest number that sounds impressive. Start with the number you can live with.

Good starter points:

- 5 percent of each paycheck if money feels tight

- 10 percent if your bills are steady and you have some room

- A flat $25, $50, or $100 per paycheck if percentages feel abstract

If your income varies, a percentage usually works better. If your income is stable, either method is fine.

Step 2: Open or choose a separate high-yield savings account

Keep this savings account separate from your everyday checking. Out of sight helps. You want enough distance that spending from it feels like a conscious choice, not a reflex.

Step 3: Set the split

If your employer offers split direct deposit, log into your payroll portal or ask HR how to set it up. You may be able to send a flat amount or percentage directly to savings.

If not, create an automatic transfer through your bank for the same day your paycheck lands.

Step 4: Test it for one or two pay cycles

This part is important. You are not making a lifelong vow. You are running a small experiment.

After one or two paychecks, ask yourself:

- Did I still cover my bills?

- Did I need to pull money back from savings?

- Did checking feel too tight, or just slightly leaner?

Step 5: Increase slowly

If the test went fine, bump it up a little. Try another 1 percent to 2 percent, or another $25 per paycheck.

This is the part most people skip. They think saving has to start big to count. It does not. Small increases are easier to stick with, and sticking with it is what builds real results.

How to do this without killing your fun money

People hear “save first” and assume it means “stop enjoying life.” That is usually why new saving plans fail. They feel like punishment.

Do the opposite. Protect a little fun money on purpose.

If you know you like coffee runs, takeout on Fridays, or a small weekend budget, build that into your checking plan. The goal is not to become a robot. The goal is to make saving automatic while leaving enough room for normal life.

A good rule is this: if your split forces you to use a credit card for regular weekly spending, it is too aggressive for now. Dial it back and try again.

Fixed amount vs percentage: which is better?

Choose a fixed amount if:

- Your paycheck is predictable

- You like simple numbers

- You want total control over cash flow

Choose a percentage if:

- Your hours or income change

- You get overtime, commissions, or side-income deposits

- You want the habit to scale automatically when pay goes up

For many people, percentages are the easiest long-term move. You never have to rethink the math after every raise. The savings amount just grows with your income.

A simple graduated plan that feels painless

If you want a no-drama system, try this:

- Paychecks 1 and 2: save 5 percent

- Paychecks 3 and 4: save 7 percent

- Month 2 or 3: move to 10 percent if it still feels okay

That slow ramp matters. It gives your spending habits time to adjust without making you feel deprived.

You can also use raises, tax refunds, or paid-off subscriptions to increase your split. If a monthly bill disappears, redirect that amount to savings instead of absorbing it into lifestyle creep.

Common mistakes to avoid

Starting too high

If your first split causes panic, you will turn it off. Small and repeatable beats ambitious and short-lived.

Using the same account for everything

If your emergency fund sits in the same account as your daily spending money, it is too easy to blur the lines.

Checking the balance every day

Automation works best when you leave it alone. Let a few pay cycles pass before you judge the results.

Forgetting upcoming bills

Before you set your split, glance at the next month. Car insurance, annual fees, birthdays, and school expenses have a way of sneaking up on people.

What this can look like in real life

Let’s say you bring home $2,000 every two weeks.

- At 5 percent, you save $100 per paycheck

- That is $200 a month

- In 6 months, that is about $1,200 plus interest

- In 12 months, that is about $2,400 plus interest

Now imagine you increase it to 8 percent after two months because the first level felt manageable. Suddenly the account starts looking like a real emergency buffer, not just a symbolic savings attempt.

That is the quiet power here. Not one giant heroic move. Just a habit that repeats often enough to matter.

When this habit works best

This system is especially useful if:

- You tend to spend what you see in checking

- You hate budgeting apps and spreadsheets

- You want to save without making daily decisions

- You are waiting for the “right time” to get serious about saving

The right time is usually your next paycheck.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Fixed amount split | Sends the same dollar amount from every paycheck to high-yield savings. Easy to plan around if income is steady. | Best for predictable paychecks and simple budgeting. |

| Percentage split | Moves a set percentage of each paycheck, so savings rises and falls with your income automatically. | Best for variable income or anyone who wants the habit to grow naturally over time. |

| Manual leftover saving | Waits until the end of the pay cycle to save whatever remains, if anything remains. | Least reliable. Too dependent on willpower and surprise expenses. |

Conclusion

The paycheck split high yield savings habit works because it removes the hardest part of saving, which is having to decide over and over again. With rates still attractive and budgets stretched, this is one of those rare money moves that is both simple and useful. Pick a fixed amount or a percentage. Test it for one or two pay cycles. If it feels fine, increase it a little and keep your fun money intact. That is it. No spreadsheet marathon. No waiting for a raise. Just a small, repeatable system that turns your very next paycheck into a better savings routine and, over the next 6 to 12 months, into real progress.