The ‘Savings Buckets Map’: One 30-Minute Setup That Makes Your HYSA Feel Like Five Paychecks

You did the responsible thing. You opened a high yield savings account. The problem is, it can still feel like a giant blob of money with no personality and no plan. One transfer goes in, another comes out, and before long you are staring at the balance wondering, “Wait, how much of this is actually for emergencies, and how much was supposed to be for that trip?” That fuzzy feeling is what makes saving feel boring, and sometimes even pointless. A simple high yield savings account buckets strategy fixes that fast. In about 30 minutes, you can turn one account into a clear map of mini-paychecks for different parts of your life. Emergency money stays emergency money. Vacation money feels spendable. Future-you still gets funded. Best of all, you do not need a fancy app or a bank with special features. A notes app, spreadsheet, or even one sheet of paper can do the job.

⚡ In a Hurry? Key Takeaways

- A high yield savings account buckets strategy means giving one savings account several clear jobs, like emergencies, fun, and short-term repairs.

- Set up 3 to 5 buckets, assign each a target amount, and split every deposit by percentage or dollar amount so saving feels visible and useful.

- Keep true emergencies separate from fun and near-term spending, so you are less likely to drain long-term savings when normal life happens.

Why one big savings pile feels so weird

Money is emotional. A single balance number does not tell your brain much. It just sits there, looking both too small and too available.

That is why people raid savings for random expenses. Not because they are irresponsible, but because unassigned money feels like spare money.

A buckets map changes that. It gives every dollar a label and a purpose. Once that happens, your HYSA stops feeling like a black hole and starts feeling like progress.

What a buckets map actually is

Think of it as a cheat sheet for your savings account.

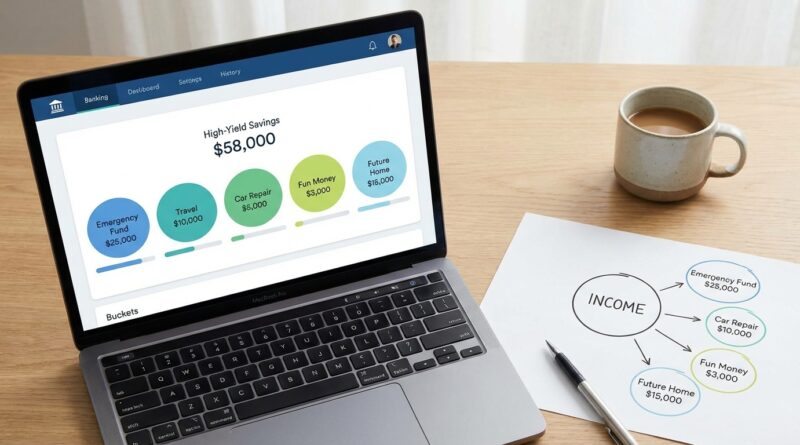

You keep one HYSA, or use a bank with built-in buckets if yours offers them, and divide the balance into categories such as:

- Emergency fund

- Car or home repairs

- Travel

- Holiday or gift fund

- Fun money

- Future-you goals

The money can live in one account or in separate sub-accounts. The important part is the map. You need a simple place to track what portion belongs to what.

The 30-minute setup

Step 1: Pick 3 to 5 buckets

Do not start with twelve. That sounds organized, but it gets annoying fast.

A good starter setup looks like this:

- Emergency: Job loss, urgent medical costs, major surprise bills

- Life Happens: Car tires, vet bill, home repair, school fees

- Fun: Weekend trip, concert, hobbies, guilt-free splurges

- Future Goal: Next apartment, new laptop, down payment, big personal goal

If you want a fifth, add Annual Bills for things like insurance premiums, holiday spending, or subscriptions that hit all at once.

Step 2: Give each bucket a target

Targets turn vague wishes into real goals.

Examples:

- Emergency: $5,000 or 3 to 6 months of basic expenses

- Life Happens: $1,000

- Fun: $600

- Future Goal: $3,000

- Annual Bills: $1,200

You do not need perfect numbers. Start with “good enough” numbers and adjust later.

Step 3: Split incoming money on purpose

This is the part that makes the system feel like five paychecks.

Every time money lands in savings, divide it the same way. For example:

- 50% to Emergency

- 20% to Life Happens

- 10% to Fun

- 20% to Future Goal

Or use flat amounts:

- $100 to Emergency

- $40 to Life Happens

- $20 to Fun

- $40 to Future Goal

Consistency matters more than the exact split.

Step 4: Track it somewhere simple

If your bank has built-in buckets, great. Use them.

If it does not, make a basic tracker in:

- Your phone notes app

- A Google Sheet

- A paper notebook

It can be as simple as this:

- Emergency: $1,850

- Life Happens: $450

- Fun: $220

- Future Goal: $780

Add them up. They should equal your HYSA balance.

What makes this work so well

It reduces friction. Instead of asking, “Can I afford this?” you ask, “Which bucket is this for?”

That is a much cleaner question.

If your car battery dies, the money comes from Life Happens. You do not feel like you failed and “broke into savings.” You used the exact money that was set aside for boring surprises.

If you book a cheap beach weekend from the Fun bucket, you can actually enjoy it. No guilt spiral. No pretending all spending is bad.

Why separate emergency money from normal surprises

This is the part many people skip.

Not every unexpected expense is an emergency. New brakes, a cracked phone screen, or a last-minute school expense are annoying, but they are regular life.

If you dump everything into one savings pile, those costs end up eating the same money you meant for true emergencies.

That is why a “Life Happens” bucket is so useful. It acts like a shock absorber.

If your bank does offer buckets, use them carefully

Some banks now let you label savings goals inside the account. That is handy, but do not assume the tool will do the thinking for you.

You still need clear rules:

- What counts as an emergency

- What bucket each transfer goes into

- What target amount you are trying to hit

- Which buckets get paused once they are full

The feature is nice. The plan is what matters.

A simple example of the map in real life

Let’s say your HYSA balance is $4,000.

- Emergency: $2,500

- Life Happens: $700

- Fun: $300

- Future Goal: $500

Then your dog needs a vet visit that costs $280.

Without buckets, it feels like your savings just shrank. With buckets, you know exactly what happened. Life Happens drops from $700 to $420. Everything else stays mentally protected.

That clarity is what keeps people saving.

How to keep the system from getting messy

Do a 5-minute check once a month

Open the account, compare the balance with your tracker, and adjust any bucket totals after spending or deposits.

Rename buckets when life changes

Your “Holiday” bucket can become “Move Fund.” Your “Fun” bucket might become “Summer Trips.” The names should match your real life, not some perfect budgeting template.

Do not create tiny buckets for every possible event

You do not need separate funds for oil changes, birthdays, concert tickets, and cousin weddings. That is how people quit.

Keep it broad enough to be easy.

What to do when you are tempted to steal from one bucket

First, be honest. Sometimes you do need to move money around.

But if you are constantly grabbing from Future Goal or Emergency to pay for impulse buys, the issue may not be your savings setup. It may be the stuff trying to lure your money away in the first place.

That is where a habit like The 15-Minute ‘Deal Detox’ Habit: How To Turn Missed Bargains Into High-Yield Savings Wins fits in nicely. It helps you turn that “I almost bought it” energy into an actual transfer to savings instead.

Best buckets for most people

If you want a plug-and-play high yield savings account buckets strategy, start here:

- Emergency: True crisis money

- Life Happens: Repairs, bills, and random real-world annoyances

- Fun: Guilt-free spending that keeps life enjoyable

- Future Goal: Bigger next-step plans

That setup covers most households without turning your savings into a spreadsheet hobby.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| One big HYSA balance | Simple to open, but hard to tell what money is meant for what goal | Easy to start, harder to stick with |

| HYSA with bucket labels or sub-accounts | Lets you divide savings into clear jobs like emergency, travel, and repairs | Best for motivation and clarity |

| Manual buckets map | Use one HYSA plus a note, spreadsheet, or notebook to track each category | Works almost as well, and costs nothing |

Conclusion

Most savings advice stops at “open a high-yield savings account,” which is only the first step. The part that makes it feel real is giving the money jobs you can actually see. A buckets map does exactly that. One pool for emergencies. One for guilt-free fun. One for near-term goals like a car repair or weekend away. That structure helps you avoid raiding long-term savings every time life gets noisy, and it makes saving feel more motivating because you can tell what your money is doing. The best part is that you can copy this system in about 30 minutes, even if your bank does not offer fancy built-in buckets. One account. A few labels. A lot less stress.