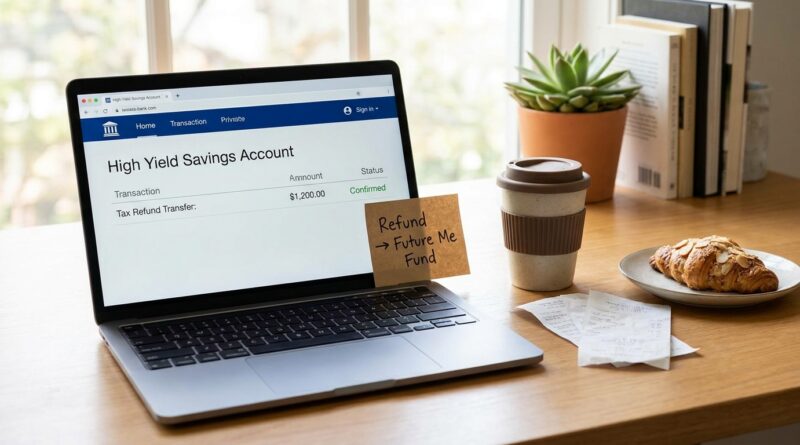

The ‘Tax Refund To HYSA’ Habit: Turn This Year’s Windfall Into Next Year’s Safety Net

Your tax refund has a funny way of disappearing. It lands in checking, you feel briefly rich, and then life happens. A weekend trip. A few food deliveries. That one thing you have been putting off buying. A week later, the balance looks almost the same as before, and the one chunk of money that could have helped you breathe easier is gone. If that sounds familiar, you are not bad with money. You are just dealing with a system that makes spending easy and saving feel optional. The fix is simple. Treat your refund like a split deposit, not a bonus. Send a set percentage straight into a high yield savings account, preferably at a separate bank, before your checking account gets first crack at it. Then add a small weekly transfer so this year’s refund becomes the start of next year’s safety net, not a short-lived shopping spree.

⚡ In a Hurry? Key Takeaways

- Use a tax refund high yield savings habit by moving a fixed percentage of your refund straight into a HYSA as soon as it arrives.

- Keep that account at a separate bank and add a $10 to $25 weekly auto-transfer so the refund turns into an ongoing savings routine.

- Rates are still relatively strong, even if they are drifting down, so leaving refund money idle in checking costs you both interest and future peace of mind.

Why your refund disappears so fast

Checking accounts are built for motion. Bills come out. Swipes happen. Subscriptions renew. If your refund lands there, it gets mixed in with everyday money and starts feeling spendable almost immediately.

That is the real problem. Not willpower. Visibility.

When money sits in the same place as groceries, gas, and impulse buys, your brain stops treating it like a chance to get ahead. It becomes part of the blur. That is why a tax refund high yield savings habit works so well. It changes where the money lives before you can slowly chip away at it.

The simple habit that actually sticks

Here is the play: decide in advance what percentage of your tax refund goes to savings. Then move that amount into a high yield savings account the same day the refund hits, or better yet, as soon as you know it is coming.

Pick a percentage, not a vague goal

Saying “I should save some of this” is too fuzzy. Pick a number. For most people, one of these works well:

- 25% if money feels tight and you still want room to enjoy some of the refund

- 50% if you want a real cushion without going full monk mode

- 75% or more if you are behind on emergency savings and want to catch up fast

The point is not perfection. The point is deciding before the money arrives.

Use a separate bank

This matters more than people think. If your HYSA is at the same bank as your checking account, moving money back is usually too easy. A separate bank adds a little friction. Not enough to block you in a real emergency, but enough to stop random “I deserve this” transfers.

That tiny speed bump is often what saves your savings.

Stack a weekly transfer on top

This is the part that turns a one-time move into a lasting habit. Once your refund money is in the HYSA, set up an automatic weekly transfer of $10 to $25. Small enough to live with. Big enough to keep momentum going.

If you want a low-stress way to build that first layer of cash cushion, this pairs nicely with The 15-Minute ‘Mini Emergency Fund To HYSA’ Habit: Build Real Safety Without Killing Your Fun Money.

Why this works better than trying to “be good”

Good systems beat good intentions. Every time.

A refund is one of the few moments in the year when a larger chunk of cash shows up at once. That makes it powerful. But only if you give it a job quickly. Putting part of it in a HYSA does three useful things at once:

- It gets the money out of your spending lane

- It lets the balance earn more interest than a standard savings or checking account

- It creates a visible emergency cushion, which lowers stress fast

And right now, that matters. Rates on high yield savings accounts are still historically solid, even though they have started to drift down from peak levels. That means idle cash in checking is doing even less for you while prices still feel high.

How much could this really help?

More than it seems.

Let’s say your refund is $2,000. If you send 50% to a HYSA, that is $1,000 saved immediately. Then you add $20 a week. Over a year, that is another $1,040, not counting interest. Now your spring refund has quietly turned into a little more than $2,000 in savings momentum.

That is the difference between panicking over a car repair and handling it. Between putting an unexpected bill on a credit card and paying it in cash.

How to set this up in 15 minutes

1. Choose the percentage before the refund arrives

Make the call now. Do not wait until the money is sitting in checking, looking friendly.

2. Open or use a HYSA at a separate bank

Look for no monthly fees, FDIC or NCUA insurance, and easy transfers. You do not need the absolute top rate on earth. You need a solid account you will actually use.

3. Move the money right away

The same day is best. If the refund already landed, do it now before the “small treats” add up.

4. Set a weekly auto-transfer

Pick $10, $15, $20, or $25. Start small if needed. A transfer you can keep is better than an ambitious one you cancel in a month.

5. Name the account something specific

Try “Emergency Cushion,” “Car and Life Stuff,” or “Do Not Touch Unless It Is Real.” Names help. Seriously.

Common mistakes to avoid

Saving whatever is left over

This rarely works because “left over” tends to mean “gone.” Save first, then spend the rest guilt-free.

Putting the full refund into checking “for now”h4>

That “for now” window is where the money disappears. Split it fast.

Choosing a transfer that is too big

If $25 a week feels tight, do $10. Habits survive on realism.

Chasing tiny rate differences and never opening the account

A decent HYSA today beats the perfect HYSA you research for three more weeks.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Refund location | Checking makes the money easy to spend. A separate HYSA keeps it out of your daily flow. | HYSA wins for protection and follow-through. |

| Savings method | A fixed percentage of the refund gives you a clear rule. “I will save what is left” usually fails. | Pick a percentage in advance. |

| Keeping the habit going | A $10 to $25 weekly auto-transfer keeps the balance growing long after tax season ends. | Small automation is the secret sauce. |

Conclusion

If the world feels shaky and everything feels expensive, this is one of those rare money moves that is both simple and genuinely useful. Rates on high yield savings accounts are still strong by historical standards, even if they are easing a bit, so every dollar sitting idle in checking is a missed chance to build some breathing room. A tax refund high yield savings habit does not ask you to give up all the fun. It asks you to claim part of a windfall before everyday spending swallows it whole. Route a set percentage of your refund into a HYSA at a separate bank, then stack a $10 to $25 weekly auto-transfer on top. That turns one spring deposit into a year-round safety net. Small move. Real payoff. Exactly the kind of steady win that makes life feel a little less fragile.