The ‘Interest Sweep’ Habit: A 2‑Step Move That Turns Every Rate Hike Into Free Money

You are not imagining it. Savings rates keep making headlines, but when the interest lands in your account, it often feels laughably small. A few dollars here. Maybe a little more there. Then it melts into the same balance as everything else, and you never really feel the win. That is why a lot of people give up on saving, even when their high-yield savings account is actually doing better than it has in years. The fix is not saving harder. It is making the interest visible. Try an “interest sweep” habit. Step one, let your monthly interest post. Step two, move only that interest amount into a separate savings goal with a clear name, like “holiday gifts,” “next laptop,” or “summer trip.” Now every rate hike feels real. Instead of invisible pennies, you get a growing goal fund without changing your budget at all.

⚡ In a Hurry? Key Takeaways

- The best high yield savings account habit to grow interest faster is to sweep each month’s earned interest into one named savings goal.

- Check your account on the same day each month, note the interest paid, and transfer that exact amount automatically or manually.

- This does not create extra risk or require a bigger budget. It simply makes your existing interest feel real and keeps you motivated.

Why your higher savings rate still does not feel exciting

Here is the annoying part. Your bank can raise the annual percentage yield, but your brain still reads the result as “not much happened.”

That is because interest usually arrives quietly. It shows up as a line item. Then it gets absorbed into the total. No celebration. No clear progress marker. No sense that your money did anything useful.

So even when your account is earning more, it feels flat.

This is exactly why the interest sweep habit works. It turns an invisible gain into a visible move.

The 2-step interest sweep habit

Step 1: Let the monthly interest land

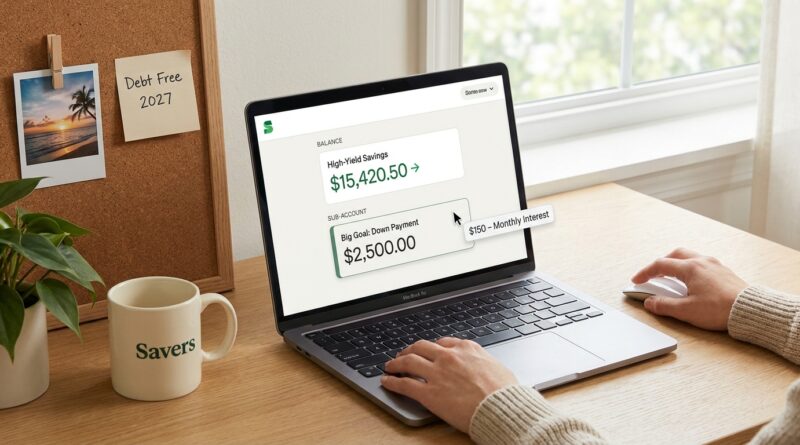

Most high-yield savings accounts pay interest monthly. You do not need to calculate anything fancy. Just wait for the bank to post the amount.

Look for a line that says something like “interest paid” or “interest credit.” That is your number.

Step 2: Move that exact amount to one named goal

Now transfer only that interest amount into a separate bucket, sub-savings account, or linked savings account with a clear purpose.

Examples:

- $18.42 goes to “Holiday Gifts”

- $27.10 goes to “Emergency Fund Boost”

- $43.88 goes to “New Phone”

The amount is not the point. The visibility is.

Once you see that your interest paid for part of something real, saving starts to feel less like waiting and more like progress.

Why this high yield savings account habit helps grow interest faster

To be clear, moving interest out of your main HYSA bucket does not magically change math by itself. The reason this habit helps you grow interest faster is behavioral.

It keeps you engaged.

When people see progress, they tend to add more money, stay consistent longer, and keep chasing better rates instead of forgetting about the account. That is where the extra growth comes from.

If you want another simple system that keeps money moving in the background, read The ‘Quiet Auto-Transfer’ Habit: Set One Weekly Move And Let High-Yield Savings Grow Itself. It pairs nicely with the interest sweep because one habit builds the balance, while the other makes the reward feel real.

How to set it up without making your life harder

Option 1: Do it manually once a month

This is the easiest starting point.

- Pick one day each month to check your HYSA.

- Find the interest amount posted by the bank.

- Transfer that exact amount to a named goal.

Put a reminder on your phone if needed. Done.

Option 2: Automate a close estimate

Some banks do not let you automatically move the exact interest amount each month. That is okay.

If your monthly interest tends to be around $25, you can set an automatic transfer for $25 into your goal bucket and adjust every few months.

It does not need to be perfect to work.

Option 3: Use savings buckets if your bank offers them

Many online banks now let you create separate goals inside one account. That is ideal.

You keep the money organized without opening a bunch of new accounts, and your “interest sweep” becomes a quick internal transfer.

Choose one goal, not five

This part matters more than people think.

If you scatter the monthly interest across too many goals, you bring back the same old problem. The progress gets too small to notice.

Pick one target for now. Something you care about and can picture.

Good choices include:

- A travel fund

- A holiday spending fund

- A car repair buffer

- Your emergency fund milestone

- A replacement tech fund for your next laptop or phone

A named goal gives your interest a job. That is what makes the habit stick.

What happens when rates go up or down

This is the nice part. The habit still works either way.

If rates go up, your monthly sweep gets bigger. That feels rewarding fast.

If rates go down, you still keep the ritual. You are still noticing your money, still building a goal, and still staying connected to your savings system.

That is much better than letting the account become background wallpaper again.

Common mistake to avoid

Do not turn the interest sweep into spending permission too early.

The goal is to make progress visible, not to drain your savings every month for random treats. If your named goal is “weekend fun,” that can work for some people, but longer-term goals usually create more lasting motivation.

Also, do not obsess over moving the money the same day interest hits. Monthly consistency beats perfect timing.

Who this works best for

This habit is especially useful if you:

- Already have a high-yield savings account but feel underwhelmed by it

- Keep hearing about better rates and want to stay motivated

- Struggle to feel progress unless you can see a goal grow

- Do not want to change your current budget

It is small. But that is the point. Small habits are the ones people actually keep.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Setup effort | One monthly reminder or a simple recurring transfer into a named goal bucket. | Very easy to start |

| Impact on motivation | Turns hidden interest into visible progress, which helps you stay engaged and keep saving. | High value for almost no effort |

| Budget impact | Uses money your account already earned, so you are not increasing your monthly expenses. | Low pressure and sustainable |

Conclusion

Right now, high-yield savings rates are the highest many savers have ever seen. That means the gap between what your money could be doing and what it is actually doing has rarely been wider. Most people let those extra dollars dissolve back into the general balance where they do not feel real, so they decide saving is “not working” and slowly lose interest. The interest sweep fixes that with almost no friction. By turning each month’s interest into a visible transfer toward one named goal, you build a reward loop into your account. Better rate, bigger sweep. More consistent saving, bigger goal boost. It is a tiny behavior change, but it makes your savings feel alive again. And that is often what keeps a good money habit going long enough to matter.