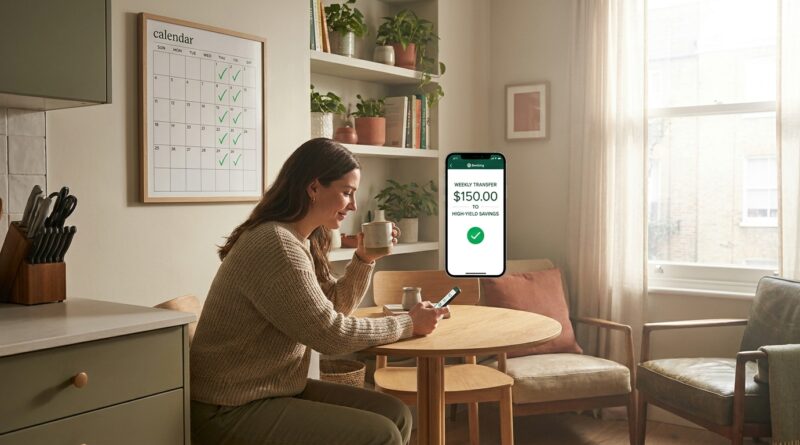

The ‘Quiet Auto-Transfer’ Habit: Set One Weekly Move And Let High-Yield Savings Grow Itself

You do not need another budgeting lecture. You need one money task that keeps working when you are busy, tired, or just not in the mood to think about bank rates. That is why the quiet auto-transfer habit works so well. Instead of checking savings apps, comparing every new promo, or promising yourself you will move money “this weekend,” you set one automatic weekly transfer from checking to a high-yield savings account and let it run in the background. That one move does two helpful things at once. It gets your cash out of a low-interest account, and it builds savings without asking you to make the same decision over and over. The best part is that weekly feels small enough to live with. You are not freezing your spending. You are just giving your future self a head start, one repeatable transfer at a time.

⚡ In a Hurry? Key Takeaways

- A simple automatic weekly transfer to high yield savings habit is often the easiest way to save more without micromanaging your budget.

- Start with a small weekly amount, like $10 to $50, scheduled for the day after payday so it happens before extra spending does.

- Pick one solid FDIC- or NCUA-insured account with a competitive rate, then leave it alone unless the rate becomes clearly uncompetitive.

Why this habit works better than “trying harder”

Most savings plans fail for a boring reason. They ask too much of your attention.

You mean to move money. Then life happens. A grocery run, a group dinner, a subscription renewal, a long workday. Suddenly the month is gone and the transfer never happened.

An automatic weekly transfer to high yield savings habit fixes that by removing the daily debate. You decide once. The bank handles the rest.

This is not about perfect discipline. It is about making savings boring in the best possible way.

Why weekly beats monthly for a lot of people

Monthly transfers sound neat on paper, but weekly transfers often feel easier in real life.

Weekly feels smaller

$25 a week can feel much less painful than $100 once a month, even though the math is the same. Smaller moves are easier to live with, so you are less likely to cancel them.

Weekly builds momentum faster

You see progress four or five times a month instead of once. That little mental win matters. Savings starts to feel active, not stalled.

Weekly helps protect cash before it gets spent

Money sitting in checking has a way of getting assigned to takeout, random online carts, and “why not” purchases. A weekly sweep cuts down on that drift.

How to set up the habit in about 15 minutes

You do not need a spreadsheet marathon. Just do these steps once.

1. Pick one high-yield savings account

Do not chase every flashy promo. Look for a bank or credit union with a competitive annual percentage yield, no monthly fee, and solid transfer tools. Also make sure it is FDIC-insured or NCUA-insured.

2. Link your checking account

This is usually done through the savings bank’s website or app. You will verify the account, often with micro-deposits or a secure sign-in.

3. Choose a small starting number

If you are unsure, start lower than you think. $15, $20, or $25 a week is enough to build the habit. You can always raise it later.

4. Schedule it for the day after payday

This is the sweet spot. Your paycheck lands, bills begin to clear, and your transfer slips out before the rest of the money starts looking available.

5. Name the account something useful

Try labels like “Emergency Buffer,” “House Repairs,” or “Next Car.” Specific names make the account feel real and less tempting to raid.

What if rates keep changing?

They will. That is normal.

But here is the trap. People spend so much time hunting for the absolute top rate that they never open anything at all. Meanwhile, their money keeps sitting in a traditional savings account earning almost nothing.

Getting a good high-yield account open matters more than squeezing out every last decimal point. If your account is competitive and fee-free, you are already doing far better than letting cash idle at a big bank’s tiny rate.

Think of this as “good enough to start, smart enough to keep.” Not “optimize forever.”

How much difference can it really make?

More than many people expect.

There are two wins happening at once. First, you are contributing regularly. Second, the money is sitting in an account that may pay several times more than a standard brick-and-mortar savings account.

Even if your weekly amount is modest, the habit does heavy lifting because it keeps money moving in the right direction all year long. You are not relying on leftover cash. You are creating it.

The mistake to avoid: making the transfer too ambitious

This is where good intentions go to die.

If you set the transfer too high, it will start bumping into groceries, gas, and real life. Then you will resent it, turn it off, and tell yourself you will restart later.

Start with an amount that feels almost boring. A transfer you barely notice is more powerful than a heroic transfer you cancel in three weeks.

After a month or two, check your checking account balance patterns. If you are consistently comfortable, increase the weekly amount by $5 or $10.

When this works especially well

This habit is great for people who:

- Get paid regularly and want a low-effort savings system

- Keep too much cash in checking and spend it by accident

- Feel overwhelmed by budgeting apps and constant money tracking

- Want to save without cutting every small pleasure

If going out with friends tends to wreck your best intentions, pair this habit with The ‘Social Swap’ Habit: Cut Going‑Out Costs Without Cutting Your Social Life. It is a smart way to reduce social spending pressure without becoming the person who always says no.

What about emergencies or needing the money back?

This is savings, not exile.

Your money is still yours, and high-yield savings accounts are designed to stay accessible. Transfers back to checking can take a little time depending on the bank, so this setup adds just enough friction to stop impulse spending without making your cash unreachable.

That said, you still want a cushion in checking. Do not drain it to the bone. The goal is to move extra money into a better-paying home, not create overdraft stress.

A simple rule for picking your weekly number

Use this easy test.

Choose an amount that would not cause panic if it left your account every week for the next two months.

For many people, that means:

- $10 a week if money is tight

- $25 a week if you want a gentle start

- $50 a week if your budget has a bit more room

The right number is the one you can keep.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Weekly auto-transfer size | Small recurring amounts like $10 to $50 are easier to sustain than one large monthly move. | Best for consistency |

| Chasing the top rate | Constantly switching for tiny rate differences often creates delay and mental clutter. | Usually not worth it |

| One solid high-yield account | Competitive APY, no monthly fees, and FDIC or NCUA insurance give you most of the benefit with less hassle. | Smart default choice |

Conclusion

You do not need to become a part-time rate hunter to make this work. Right now, top high-yield accounts are quietly paying several times more interest than big traditional banks, but most people never see the benefit because they keep meaning to “get around to it” and never do. A tiny, repeating weekly transfer into one solid high-yield account turns today’s rate environment into a stress-free win. You build momentum, protect your money from low-yield accounts, and still spend freely from your normal checking because the decision was already made once, not every day. Quiet habits are often the ones that stick. This is one of them.