The ‘Savings Lane-Split’ Habit: Park Your Cash In A High-Yield Account Without Changing How You Spend

You are not lazy if you have not opened a high-yield savings account yet. You are busy. For a lot of people, the problem is not knowing that better rates exist. It is the annoying part after that. New login. New app. Identity checks. Linking accounts. Wondering which bills might break if you move too much too fast. So the money stays in the old savings account earning almost nothing, while plenty of banks are paying 4 to 5 percent. The good news is you do not need a full bank breakup to fix this. A simple “savings lane-split” works well. Keep your checking account and normal spending exactly where it is. Then open one high-yield savings account as a parking spot for extra cash and set up automatic transfers. That is it. You get most of the benefit without rebuilding your whole money system.

⚡ In a Hurry? Key Takeaways

- You can use a high yield savings account without switching banks by keeping your current checking account and linking one new savings account to it.

- Start with a small automatic transfer each payday so your extra cash moves over without changing bills, debit cards, or direct deposit.

- Focus on FDIC or NCUA insurance, no monthly fees, and easy transfers. You do not need the absolute top rate to come out ahead.

How the “savings lane-split” habit works

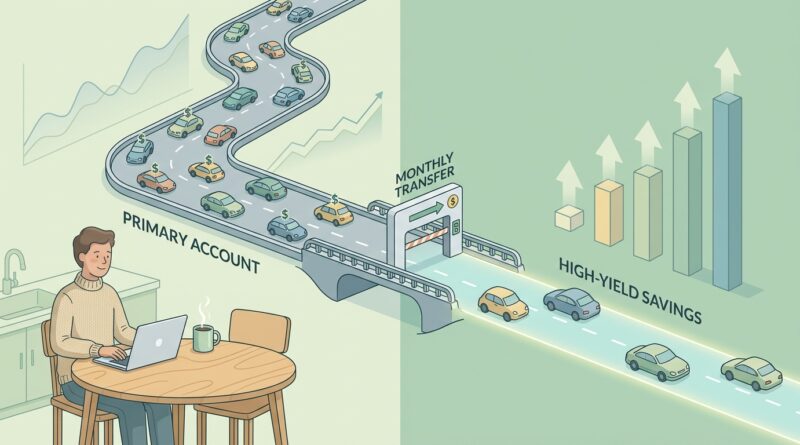

Think of your money like traffic.

Your checking account is the main road. Paychecks come in. Bills go out. Your debit card, rent, subscriptions, and autopays all keep moving like they always have.

The high-yield savings account is the side lane. It is not where you do your daily spending. It is where you park money that does not need to be touched this week.

That is the whole idea behind how to use a high yield savings account without switching banks. You do not replace your money system. You add one better parking spot.

Why this works better than a full bank switch

Switching banks sounds simple until you picture the cleanup work. Updating payroll. Moving every autopay. Replacing saved card numbers. Watching for missed payments. It can feel like doing taxes with a headache.

A lane-split setup avoids almost all of that.

Your current checking account stays as mission control. The high-yield account has one job. Hold emergency savings, sinking funds, or extra cash at a better rate.

You get the biggest win, which is earning more on idle money, without turning the rest of your life upside down.

What to put in the high-yield account

This habit works best for money that does not need daily access.

Good choices

Emergency fund money is a perfect fit. So is a vacation fund, home repair fund, insurance deductible fund, or the cash you are holding for quarterly taxes.

If your checking account regularly carries a cushion of a few thousand dollars “just in case,” that extra buffer can often move here too, as long as you leave enough in checking for bills and normal surprises.

Not-so-good choices

Do not use it for money needed for tomorrow’s rent or a bill due this week. Transfers can take a day or two, sometimes longer at a new bank. This is a parking lane, not your wallet.

How to set it up in under 15 minutes

You do not need a spreadsheet and a 12-step money makeover. Here is the simple version.

Step 1: Pick one high-yield savings account

Look for three basics. No monthly fee. FDIC insurance if it is a bank, or NCUA insurance if it is a credit union. A competitive rate that is clearly listed.

Do not get stuck chasing every last decimal point of APY. If one account pays 4.30 percent and another pays 4.45 percent, the difference on a modest balance may be tiny. Ease of use matters too.

Step 2: Link it to your current checking account

This is usually done by entering your checking account and routing number, or by signing in through your bank’s secure linking tool.

Some banks verify with small test deposits. Annoying, yes. But it is a one-time annoyance.

Step 3: Move a starter amount

Send over a small chunk first. Maybe $250, $500, or one month of your current “just sitting there” cash. This lets you test transfers and get comfortable with the setup.

Step 4: Automate the habit

Set a recurring transfer from checking to savings. Payday is usually the easiest trigger. Even $50 or $100 every pay period is enough to make the account start doing real work.

If you want a slightly smarter version, automate a fixed amount and then do a quick monthly top-up of anything left in checking above your target cushion.

How much should stay in checking?

This is where people get nervous, and fairly so. Nobody wants an overdraft just because they got excited about a better rate.

A good starting rule is to keep one month of normal bill money in checking, plus a comfort buffer. For some people that buffer is $300. For others it is $1,000. Pick the number that lets you sleep at night.

Everything above that can be a candidate for the high-yield parking lane.

If inflation has been quietly eating away at the value of your cash, it is worth reading The ‘Inflation Gap Shuffle’ Habit: A 10‑Minute Monthly Move That Keeps Your Cash Ahead Of Rising Prices. It pairs nicely with this setup because both habits are about small, low-drama moves that keep money from sitting still.

What kind of return are we really talking about?

Let’s keep it real. A high-yield savings account will not make you rich.

But it can stop your cash from loafing around at 0.01 percent.

If you keep $10,000 in an old savings account earning basically nothing, you might make about a dollar over a year. Put that same money in a high-yield account at around 4.5 percent, and you could earn roughly $450 over a year, depending on rate changes and compounding.

That is not life-changing money. But it is real money for very little effort.

Common mistakes to avoid

Moving everything at once

Leave enough in checking so bills clear comfortably. The goal is better interest, not creating a cash-flow mess.

Obsessing over the perfect APY

Rates change. Frequently. A solid account you will actually use beats a “best rate” account you keep delaying for three months.

Ignoring transfer speed

Some online banks move money faster than others. Check transfer times and limits before you commit.

Forgetting account security

Use a strong password and turn on two-factor authentication if the bank offers it. Boring advice, but very important.

Who this habit is best for

This setup is especially useful if you like your current checking account and do not want to redo your financial life.

It is also a good fit if you:

- have direct deposit and autopays already running smoothly

- keep too much cash in checking “just because”

- want better interest without more daily money decisions

- get stuck when a financial task feels too big

When a full switch might make more sense

Sometimes the bolt-on fix is not enough.

If your main bank charges monthly fees, has terrible customer service, or pays almost nothing across all account types, a full move could still be worth it. Same if you are already planning a broader money cleanup.

But if the only thing stopping you is friction, lane-splitting is the easier win. Start there first.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Keeping your current bank | Checking, debit card, direct deposit, and autopays stay where they are. Only savings gets added elsewhere. | Best for reducing hassle |

| Automatic transfers | A fixed transfer from checking to the high-yield account each payday builds savings without extra effort. | Most effective habit to start |

| Rate chasing vs. simplicity | The top APY can change often. A good insured account with no fees is usually enough to capture most of the benefit. | Choose simple over perfect |

Conclusion

If you have been putting this off, you are not alone. High-yield rates sound great, but the friction of switching banks is real. The good news is you do not need a total money overhaul to start benefiting. Keep your regular spending exactly where it is, add one high-yield savings account as a parking lane, and automate transfers from your existing checking. That gives you most of the upside of today’s stronger savings rates without the stress, decision fatigue, or messy bank migration. One small setup session, often under fifteen minutes, can get your cash working harder while your day-to-day life stays the same.