The ‘Payday Sweep-Down’ Habit: How To Use One Weekly Reset To Keep Your High-Yield Savings Growing

Your paycheck lands. You pay rent, utilities, maybe the credit card. Then you look at checking and think, nice, I have some breathing room. A week later, that “extra” money has been shaved down by delivery fees, one-too-many Target runs, app renewals you forgot about, and those little card taps that never feel serious in the moment. It is frustrating, especially when you do have a high-yield savings account and still cannot seem to make the balance climb. The problem usually is not that you are bad at saving. It is that your money is sitting in the wrong place for too long. A weekly high yield savings habit fixes that. Think of it as a reset you do after payday and once more before the weekend. You leave enough in checking for real life, then sweep the rest to your HYSA so it can start earning more instead of quietly disappearing.

⚡ In a Hurry? Key Takeaways

- A weekly high yield savings habit means setting a checking account cap, then moving any extra to your HYSA on the same day every week.

- Start with a simple buffer, like one week of spending plus a small cushion, so you do not sweep too aggressively.

- This works best when your HYSA is for savings, not bill-paying, and when you keep enough in checking to avoid overdrafts or transfer stress.

Why this habit works so well

Most people do not empty their checking account on purpose. It just happens slowly.

Checking is designed for easy spending. That is its job. Your debit card is connected to it. Your payment apps pull from it. Your subscriptions live there. So when extra cash sits in checking, it starts to feel available, even if you meant to save it.

A weekly high yield savings habit creates a little friction in the right place. It moves money out of your spending lane and into your earning lane.

That matters right now because high-yield savings accounts are still paying meaningfully more than standard checking accounts. Money in checking often earns almost nothing. Money in a HYSA at least gets a chance to grow while it waits.

What a “payday sweep-down” actually is

This is not a complicated budgeting system. It is a simple weekly reset.

You pick a target amount to keep in checking. That number should cover your upcoming bills, your normal spending, and a small cushion. Then, once a week, you check your balance. Anything above your target gets swept to your high-yield savings account.

That is the whole idea.

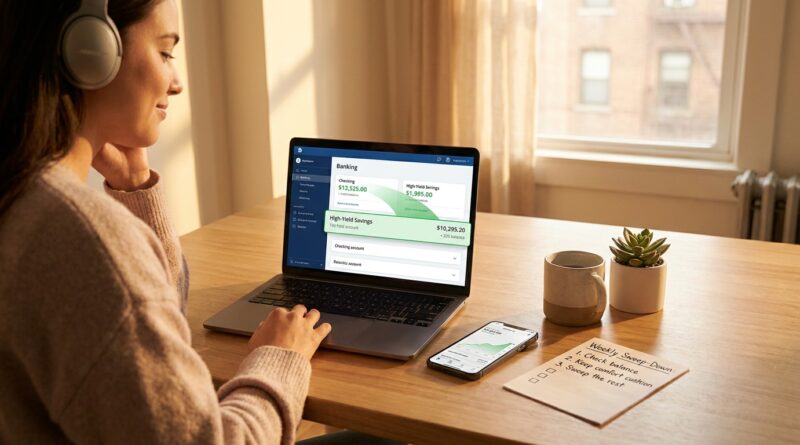

A simple example

Let’s say your checking account target is $1,200.

On Friday morning, after your paycheck and bill payments settle, your checking balance is $1,760. You move $560 to your HYSA. Now your checking is back at $1,200, which is enough for groceries, gas, and the usual week ahead.

The point is not to make checking as low as possible. The point is to stop treating every extra dollar as spendable.

How to set your checking “cap” without guessing

This is where people get stuck. They either leave way too much in checking or sweep so much that they panic three days later.

Try this instead.

Step 1: Add up one week of real spending

Look at the last month of checking activity and find your average weekly outflow. Include groceries, gas, transit, child expenses, and the random little things that happen in real life.

Step 2: Add known bills that will hit before your next paycheck

If your phone bill or streaming bundle is coming out next week, count it.

Step 3: Add a cushion

For most people, a cushion of $100 to $300 is enough to avoid stress. If your income varies or your expenses bounce around a lot, make the cushion bigger.

That total is your checking cap.

Do not aim for perfection on day one. Pick a number, test it for a month, then adjust.

When to do the sweep

The best time is the same time every week.

For many people, that is payday afternoon or the morning after payday, once direct deposit has landed and any big automatic payments have cleared.

You can also do a second mini-reset before the weekend. Weekends are where a lot of “just this once” spending lives.

A good rhythm looks like this

Friday: paycheck arrives, bills settle, sweep extra cash to HYSA.

Wednesday or Thursday: quick balance check, move any surprise extra over if you are still above your cap.

This takes five minutes once you get used to it.

Why weekly beats “I’ll save what’s left at the end of the month”

Because there usually is not much left at the end of the month.

Monthly saving sounds sensible, but it gives lifestyle creep and subscription creep far too much time to nibble away at your money. A weekly high yield savings habit shortens that window.

It also helps if you are someone who feels deprived by super-strict budgeting. You are not banning every coffee or every dinner out. You are just making sure your extra cash gets out of reach before it leaks away.

If you like the idea of automating the small stuff too, this pairs nicely with The ‘Round‑Up & Reroute’ Habit: Turn Every Swipe Into Automatic High‑Yield Savings, which catches spare change while your weekly sweep handles the bigger dollars.

How to make the habit easy enough to stick with

The best money habit is the one you will actually repeat.

Use a recurring reminder

Set a calendar alert called “Sweep checking to HYSA.” Put it on the same day each week.

Keep your HYSA linked and ready

If transfers take too many steps, you will put it off. Make sure your accounts are linked and tested in advance.

Rename your savings account

“Emergency Fund,” “Next Car,” or “House Buffer” works better than plain “Savings.” Specific names make it easier to protect the money.

Do not obsess over interest math

Yes, every dollar can earn more in a HYSA than in checking right now. But the bigger win is behavioral. You are reducing the amount of money available for casual spending.

Common mistakes to avoid

Sweeping too much, too fast

If you keep pulling money back from savings every few days, your cap is too low. Raise it. The goal is consistency, not punishment.

Using the HYSA like a second checking account

If money goes in and out constantly for everyday spending, the habit loses its power. Savings should be a parking spot, not a pass-through lane.

Ignoring timing

Pending card charges, auto-pay dates, and weekend spending matter. Build your sweep around how your money actually moves.

Forgetting annual or irregular costs

School fees, gifts, memberships, and insurance deductibles can blow up a too-tight checking plan. If those hit often enough, build a separate sinking fund for them.

Who this works best for

Honestly, almost anyone who gets paid regularly and tends to keep too much in checking.

It works if you budget carefully. It works if you hate budgeting. It works if your income is modest, because the habit is based on what is left above your needed buffer, not on hitting some big dramatic savings number.

It is also useful for people who feel guilty spending money. A sweep-down lets you save first, then use what remains in checking without second-guessing every small purchase.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Weekly sweep-down | Move any checking balance above your preset cap into your HYSA once a week. | Best balance of simple, flexible, and effective. |

| End-of-month saving | Wait until month-end to see what is left after everyday spending and surprise charges. | Easy to understand, but often leaves little to save. |

| Checking account buffer | A set amount for bills, weekly spending, and a cushion to avoid overdrafts. | Essential for making the habit safe and sustainable. |

Conclusion

The real win here is not just the interest, though that matters. Right now, rates are still meaningfully higher on high-yield savings than on standard checking, so every dollar you leave sitting in your day-to-day account is quietly earning less than it could. A simple, repeatable sweep-down ritual uses a very human truth. Most of us keep more in checking than we actually need, and then rising everyday prices, subscriptions, and impulse spending eat away at the rest. A weekly high yield savings habit gives you a practical reset that works at almost any income level and with almost any budgeting style. You do not have to say no to every small joy. You just need a system that moves your future money before your present habits can spend it.